Case Study

Strategic Case Study

Every property acquisition is more than a transaction.

Each decision influences more than just price.

• It affects leverage.

• Borrowing capacity.

• Risk exposure.

• Lifestyle alignment.

• Long-term portfolio momentum.

The following case studies demonstrate how structured thinking, financial clarity, and strategic positioning influence outcomes.

Names and minor details have been adjusted for privacy.

The principles remain unchanged.

These are not stories of luck.

They are examples of preparation, discipline, and capital allocation strategy.

Real Decisions.

Real Outcomes.

Case Study #01

Case Study #01

From $50,000 Invested to $200,000 Created

Strategic Acquisition | July 2024

Leverage rewards positioning.

This case study demonstrates the difference between automated estimates and real market evidence — and how correct asset selection compounds outcomes.

An investor believed their property was worth $620,000.

That figure came from an online estimator.

Recent comparable sales told a different story - $700,000!

A $200,000 uplift in under two years.

$50,000 invested.

$200,000 created.

This case shows how valuation accuracy and structured leverage accelerate portfolio momentum.

→ Read how positioning created a 400% return on cash invested.

Case Study #01 - Estimate vs Evidence: A $200,000 Case Study

The $80,000 Estimation Gap

Why Online Valuations Can Mislead Investors

The Acquisition

In July 2024, we secured an apartment for $500,000.

The client — Henry — contributed $50,000 as his deposit.

The rest was structured to optimise leverage.

The brief was straightforward: a low-maintenance asset in a location with genuine rental demand and the fundamentals for capital growth.

Not speculative. Just a well-reasoned buy.

February 2026 - The Portfolio Review

Nineteen months later, Henry and I caught up to review where things stood.

I asked him what he thought the property was worth.

He said $620,000, based on the realestate.com.au estimator.

Two weeks earlier, a near-identical apartment in the same complex had sold for $700,000.

Same layout. Same building. Comparable condition.

That sale wasn't an estimate — it was current market evidence.

Henry's property wasn't worth $620,000. It was worth considerably more, and he didn't know it.

The Numbers

➡️ Purchase Price (July 2024)_________________________ $500,000

➡️ Recent Comparable Sale___________________________ $700,000

➡️ Capital Growth_____________________________________ $200,000

➡️ Timeframe__________________________________________ ~19 months

➡️ Initial capital invested______________________________ $50,000

➡️ Return on cash invested____________________________ ~ 400%*

Before costs and holding expenses.

A $50,000 deposit. $200,000 in growth. That's what structured leverage looks like when the asset selection is right.

Why the estimate was wrong

Online valuation tools are algorithm-based.

They work from historical settled data, apply broad modelling across wide areas, and don't account for what's happening inside a specific complex or street.

In a fast-moving market they lag — sometimes significantly.

Henry's estimator was $80,000 short of reality. That's not a rounding error. That's a meaningful gap with real consequences for how he thinks about his portfolio.

Serious investment decisions shouldn't be based on automated estimates.

They should be based on comparable sales evidence — the same evidence a buyer's agent or valuer would use.

What the growth actually creates

A $200,000 increase in equity isn't just a number on a spreadsheet.

It's usable capital.

Henry can now refinance against that equity and use it to acquire again, hold and let it compound further, or simply understand that his position is materially stronger than he thought.

That optionality is the point of getting the asset selection right in the first place.

The Insight

Most investors make one of two mistakes with valuation.

They underestimate what they own and stay passive when they could be moving.

Or they overestimate when buying and pay too much.

Both usually come from relying on automated tools instead of actual sales evidence.

Knowing what you own — accurately — is the foundation of a functioning portfolio strategy.

Without it, you're making decisions based on a number that may have nothing to do with reality.

Key Takeaway

Property outcomes aren't accidental.

When asset selection, leverage, and market timing are aligned, the results are significant.

When they're not, you usually find out too late.

If you're not sure what your property is actually worth based on current comparable sales, that's worth finding out — not because the number will always be good news, but because you can't make good decisions without it.

This case study demonstrates the difference between:

Estimating value and Understanding value.

Considering your own portfolio position?

If you’re unsure how your property compares to recent market evidence, reviewing comparable sales may reveal opportunities you didn’t realise existed.

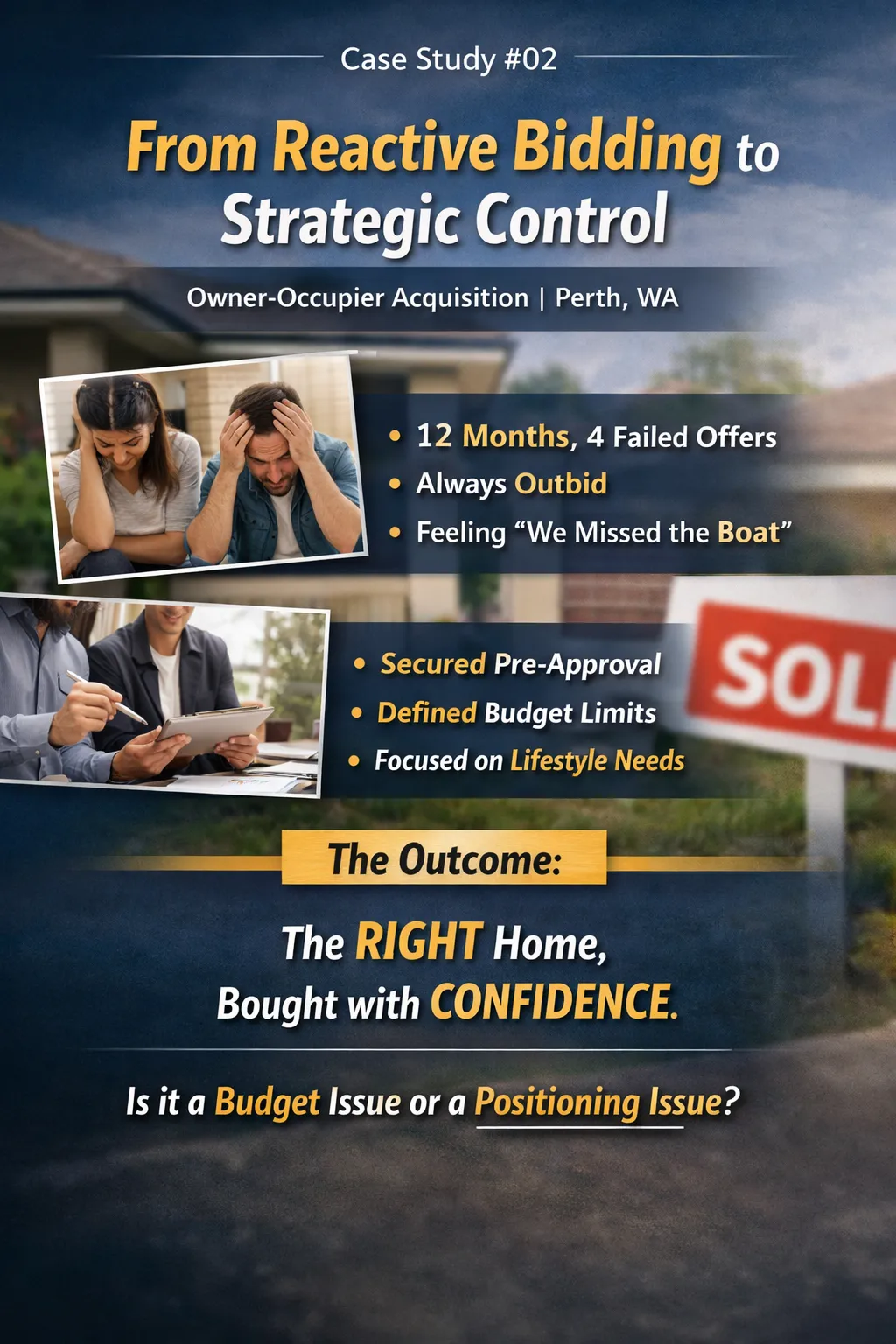

Case Study #02

Case Study #02

From Reactive Bidding to Strategic Control

Owner-Occupier Acquisition | Perth, WA

Competitive markets reward preparation.

This case study highlights the risks of emotional decision-making and the importance of financial clarity, structured negotiation, and lifestyle alignment when securing a family home.

A couple came to me after nearly a year of searching. Multiple offers submitted. Consistently outbid. To the point where they were seriously considering waiving conditions just to get something across the line.

The first thing I told them was to STOP making offers.

Not because the market was against them. Because the way they were approaching it was working against them.

This case shows how structure, clarity, and negotiation positioning transformed panic into control — and secured the right home without reckless exposure.

→ Read how preparation changes outcomes in competitive markets.

Case Study #02 - From Reactive Bidding to Strategic Control

From Reactive Bidding to Strategic Control

Competitive Market Acquisition | Perth, WA

How one couple went from 12 months of missed offers to securing the right property in under six weeks.

A couple came to me after nearly a year of searching. Multiple offers submitted. Consistently outbid.

To the point where they were seriously considering waiving conditions just to get something across the line.

The first thing I told them was to stop making offers.

Not because the market was against them. Because the way they were approaching it was working against them.

The Situation

Sarah and Mark were doing everything a buyer is supposed to do. Attending inspections, working with a broker, staying active in the market.

But 12 months in, they had nothing to show for it — and the self-doubt had started to set in.

They'd begun to believe the market had moved beyond their reach. That they'd missed the window.

What had actually happened was quieter and more fixable than that.

The decision-making environment had shifted from considered to reactive.

Offers were being made under pressure. Finance clauses were being removed. Building and pest conditions were being waived.

All in an attempt to compete — without a clear picture of what risk was being carried.

The Real Problem

When we sat down together, the structural gaps were obvious:

❌ No formal pre-approval — lending parameters were approximate, not confirmed

❌ No defined suburb focus — the search was scattered and reactive

❌ No true purchase ceiling — they didn't know their all-in acquisition cost

❌ No due diligence framework — conditions were being waived without a fallback plan

❌ No negotiation strategy — every offer was made under time pressure, property by property

Every decision was emotional. Every property felt urgent. In a competitive market, that combination is expensive.

The problem wasn't the budget. It was the structure.

What We Did First: ... STOP!

Before we looked at another property, we paused the search completely.

We worked with Sarah, Mark, and their mortgage broker to lock in three things that should have been established before the first inspection:

1. Maximum borrowing capacity — formal approval with confirmed parameters, not a rough estimate.

2. Total acquisition costs — purchase price plus stamp duty, settlement fees, inspection costs, and a contingency buffer. Most buyers anchor

on the purchase price. The real ceiling is higher.

3. A hard purchase limit — a number that would not move regardless of what happened on the day. Not a range. A ceiling.

Once those three things were in place, the anxiety that had been driving reactive decisions largely disappeared. Clarity does that.

Rebuilding the Search

With the financial framework confirmed, we rebuilt the search around what Sarah and Mark actually needed — not just what was available.

Their previous approach had been attendance-based: go to whatever came up and offer on whatever seemed close.

We replaced that with a ranked suburb list built around their life — commute, family proximity, school catchments, street quality, layout for how they actually live.

Fewer suburbs. More intentional inspections. Every visit with a purpose.

The Acquisition Framework

Once the search was defined, we implemented a structured approach to every property we assessed:

✅ Ranked micro-locations based on lifestyle fit, not just availability

✅ Clear asset selection criteria — defined before we walked through a door

✅ A non-negotiable due diligence checklist applied to every property

✅ Offers structured to be competitive without removing protections

✅ A negotiation strategy agreed in advance, so decisions weren't being made under pressure

The objective shifted from "win at any cost" to "secure correctly within defined limits."

Those are different mindsets. They produce different results.

The Outcome

Within four to six weeks of implementing the structure, Sarah and Mark secured a property in a competitive Perth suburb. Within the $800–900k range. With all conditions in place.

No protections waived. No scrambling. Settled without incident.

The market hadn't changed. The competition hadn't eased. What changed was how they showed up to it.

Why buyers keep losing — and it's usually not the budget

Most buyers who lose repeatedly assume they need to offer more. That's rarely the full picture.

There are two things that actually determine whether a prepared buyer wins in a competitive market.

The first is structure. No financial clarity, no defined ceiling, no due diligence framework, no negotiation plan. Every offer reactive. Every decision made under pressure. That's not a competitive approach — it's hoping the market goes your way.

The second is confidence. A selling agent's job is to find the most secure buyer for their vendor — not necessarily the highest offer. An offer that looks rushed, poorly structured, or financially uncertain signals risk. And vendors hesitate on risk.

A well-prepared buyer presents with clear lending evidence, defined financial parameters, and decisive terms. That reads as low-risk. And low-risk buyers win offers — even when they're not the highest number in the room.

Winning isn't just about offering more. It's about presenting as the most secure and reliable buyer.

The Takeaway

Fatigue leads to poor decisions. Pressure leads to risk. Structure restores control.

If you've been repeatedly outbid, the issue probably isn't your budget. It's your positioning, your preparation, and the process behind each offer.

Those things are fixable.

If you're currently navigating the Perth market and want to think it through, I'm happy to have a conversation.

Case Study #03

Case Study #03

From Familiar Comfort to Strategic Diversification

Investor Acquisition | Portfolio Expansion Strategy

Capital allocation determines momentum.

This case study explores concentration risk, diversification strategy, and the impact of limiting beliefs on portfolio growth.

“I only want to invest in my own suburb.”

It felt safe. It felt familiar.

But familiarity concentrated risk.

PPOR and investment tied to the same postcode.

Lower yield. Higher entry price. Slower growth runway.

This case shows how strategic diversification improved yield, preserved borrowing capacity, and protected long-term scalability.

→ Read why comfort can quietly limit performance.

Case Study #03 - From Familiar Comfort to Strategic Diversification

From Familiar Comfort to Strategic Diversification

Investor Acquisition | Portfolio Expansion Strategy

The Situation

David and Claire owned their home in Perth's western suburbs.

Good area. Strong owner-occupier demand. The kind of postcode people feel safe in.

When they came to me to buy their first investment property, the thinking was straightforward: buy nearby.

Same suburb. They knew it, they trusted it, and it had served them well.

That instinct makes complete sense.

It's also worth pushing on.

The Core Assumption

The logic was - "if the suburb has performed for us as homeowners, it should perform for us as investors".

And look — blue chip areas do have real advantages.

Stability, consistent demand, they hold up reasonably well in downturns.

I'm not here to argue otherwise.

But those same areas have characteristics that work against you when you're trying to build a portfolio rather than just buy a home.

➡️ Entry prices are high relative to what you'll earn in rent.

➡️ Yields are structurally lower.

➡️ Percentage growth tends to slow once a suburb has matured.

➡️ And if you already own your home there, you're now doubling up exposure in the same economic pocket.

Before we went any further, I ran the numbers side by side.

The Numbers

▪️Option A – Blue Chip Suburb (Home Neighbourhood)

Purchase Price_________________$1,200,000

Rental Income__________________$850 per week

Gross Yield_____________________~3.7%

Capital Exposure_______________PPOR + Investment tied to the same postcode

▪️Option B – Strategic Growth Corridor

Purchase Price__________________$650,000

Rental Income___________________$750 per week

Gross Yield______________________~6.0%

Capital Exposure________________Diversified into a separate economic and demographic pocket

That 2.3 percentage point yield gap matters week to week.

But the bigger issue is what the entry price does to their position going forward.

At $1.2 million, Option A would have consumed a significant chunk of their borrowing capacity.

A third property would have become much harder to fund.

At $650,000, Option B kept that door open.

The Concentration Risk Problem

David and Claire already had their home in the western suburbs.

Adding an investment property in the same postcode would mean both assets moving together — up, and sideways, and down.

That's not automatically wrong. But it's a risk worth naming clearly.

If that market stagnates for three to five years — which any market can do, at any point in its cycle — both properties slow at the same time.

Equity growth slows. The loan-to-value ratio improves more slowly. Borrowing capacity tightens. The next acquisition gets pushed further out.

Stagnation doesn't just affect value. It affects momentum.

And in portfolio building, lost momentum is expensive in ways that are hard to see until you're already behind.

Owning in two separate markets breaks that dependency.

If one goes sideways, the other isn't necessarily dragged with it.

The Belief That Needed Examining

"I prefer to invest where I live" is one of the most common positions I hear from first-time investors.

It comes from a reasonable place — familiarity feels like knowledge, and knowledge feels like safety.

But familiarity with a suburb as somewhere you enjoy living is not the same thing as an objective assessment of it as a place to put capital.

The western suburbs is a great place to live.

That's not the same as it being the right place for the next $1.2 million.

What They Decided

David and Claire went with Option B.

Better yield. Lower entry price. Borrowing capacity intact.

Two separate markets instead of everything concentrated in one.

The decision came down to the numbers, not postcode attachment.

The Strategic Insight

Blue chip isn't wrong.

Established suburbs offer stability and long-term resilience — those things are real.

But stability and outperformance aren't the same thing, and for a first investment property, yield efficiency and room to grow matter more than comfort.

There are markets outside the traditional postcodes delivering stronger percentage growth, better rental yields, and more runway for capital gains right now.

Limiting yourself to one suburb — without putting the numbers side by side — risks missing that.

The question for any investment decision isn't "do I know this suburb?" It's "does the data support this allocation?"

Key Takeaway

If your home and your investment property are in the same postcode and that market underperforms for five years, both assets take the hit at once.

That's a portfolio design problem, not a market problem — and it's one you can solve at the point of purchase.

Invest in blue chip if the numbers support it.

But run the comparison first.

Case Study #04

Case Study #04

From Public Competition to Private Opportunity

Off-Market Acquisition | Perth, WA

Not every property is found on the open market.

This case study highlights how a proactive approach and direct engagement can create opportunities before they are exposed to public competition.

At one home open, there were over 50 buyer groups through the property.

More than 20 offers were submitted.

The outcome was predictable.

→ Multiple offers.

→ Escalating price pressure.

→ Buyers competing emotionally.

Instead of entering that environment, we approached the market differently.

This case shows how securing an off-market opportunity removed competition, created negotiation control, and delivered a clean outcome for both buyer and seller.

→ Read how positioning ahead of the market changes the result.

Case Study #04 - From Public Competition to Private Opportunity

Off-Market Acquisition | Perth, WA

How a proactive approach secured the right property without competing for it

The Brief

After our initial meeting, the acquisition brief was clear.

Target suburb identified. Asset criteria confirmed. Financial boundaries set.

There were active listings on the market that broadly matched what the client needed. On paper, the search should have been straightforward.

It was not.

The Reality of the Public Market

At one home open I attended on the client's behalf, around 50 buyer groups came through the property.

More than 20 offers were submitted before the week was out.

The result was predictable.

Price escalation. Compressed timelines. A final figure shaped by competition rather than value.

This is what happens when a suitable property hits the public market in a tightly held Perth suburb.

Everyone sees it. Everyone inspects it. Everyone competes for it.

Winning stops being about making a smart decision and starts being about outbidding the person next to you.

That is not a position I was willing to put my client in.

The Strategic Shift

Rather than continuing to chase publicly listed properties, I took a different approach.

I reached out directly to property owners within the client's target suburb, with one objective: identify potential sellers before they formally listed and before the rest of the market had a chance to find them.

Through direct engagement with owners, I identified someone open to a conversation.

The property met the brief across every measure.

Location, layout, and budget all aligned.

And critically, it had not been seen by the open market.

The Negotiation

With no competing offers in the background, the negotiation was controlled.

Both parties had a clear understanding of value.

The conversation was straightforward, the terms were defined, and the expectations on both sides were transparent from the start.

The seller received certainty and a clean, uncomplicated transaction.

The client secured a property that suited their needs without inflated pricing or artificial pressure.

That is what a negotiation looks like when the process is set up properly.

The Outcome

The property was secured off-market.

No public campaign. No bidding war. No price escalation beyond what the numbers justified.

The client acquired the right property for their situation, on their terms.

What This Actually Takes

Off-market access in Perth is not about secrecy or insider deals.

It is about preparation and positioning.

It requires a well-defined brief, genuine relationships within the market, the willingness to do the legwork before a property appears publicly, and a buyer who is ready to move when the right opportunity presents itself.

That readiness is the part most buyers underestimate.

Access matters, but only if you are in a position to act on it.

In a competitive market, the advantage belongs to buyers who are already ahead of public exposure, not those reacting to it.

Is This Relevant to Your Situation?

If you are considering purchasing property in Perth, it is worth asking a simple question.

Are you competing with 20 other buyers, or are you positioned before the property reaches them?

If you would like to explore whether a similar approach could work for your situation, get in touch and we can have a conversation about what might be possible.

Case Study #05

Case Study #05

When Due Diligence Reveals the Real Opportunity

Investor Acquisition | Portfolio Expansion Strategy

A property listed “sold as-is” in Perth South West, WA had previous termite damage within the roof structure.

Most buyers would have immediately walked away the moment they heard the words

“termite damage” or “major structural damage.”

But after verifying the reports, confirming no active termites, and assessing repair costs, the property revealed multiple value-add pathways — including the potential to create a 4x2, add a granny flat, or pursue future redevelopment.

Negotiated purchase price: $650,000

Comparable nearby sale: $750,000

This case study shows how proper due diligence can turn perceived risk into strategic opportunity.

→ Read how understanding the full picture changed the outcome.

Case Study #05 - When Due Diligence Reveals the Real Opportunity

Investor Acquisition | Portfolio Expansion Strategy

Coming soon....

Quick Links

Social Media Links